- AccountsRecovery Daily Digest

- Posts

- Daily Digest - March 10, 2026

Daily Digest - March 10, 2026

Brought to you by: TCN | By Mike Gibb

Mike Gibb

March 10, 2026

🎂 Happy Birthday to the following: Natasha Scott of GM Financial, Kasey Hege of InterProse, and Mike Hiller of American Profit Recovery.

🎉 Congratulations for starting new positions: Timothy Patterson as EVP Deputy General Counsel - Litigation & Legal Operations at Exeter Finance.

Borrower Claims Bank Continued Robocalls After Cease-and-Desist Letter

A national bank is facing claims of violating the Telephone Consumer Protection Act and the Rosenthal Fair Debt Collection Practices Act after a borrower alleged that dozens of automated collection calls continued even after his attorney sent a cease-and-desist letter directing the bank to communicate only through counsel.

This series is sponsored by WebRecon

A MESSAGE FROM TCN

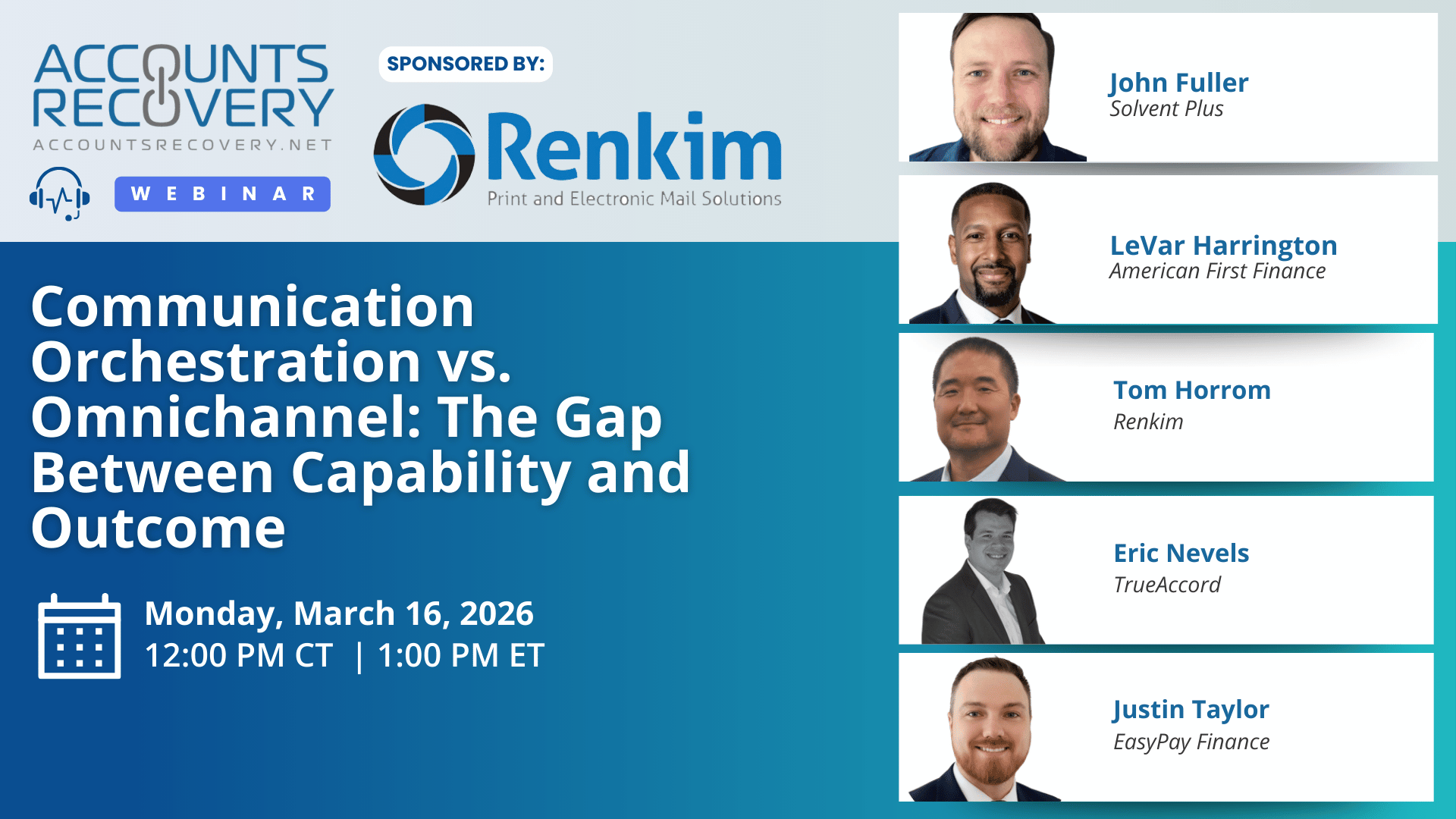

TODAY’S WEBINAR

UPCOMING WEBINARS

|  |

|  |

|

Judge Tosses ADA and FDCPA Claims Brought by Deaf Consumer Against Collector

A District Court judge in Maryland has granted a defendant’s motion to dismiss claims it violated the Americans with Disabilities Act and the Fair Debt Collection Practices Act along with state law over how it attempted to collect from the plaintiff, who is deaf. The ruling concluded that the plaintiff failed to plausibly allege that the collector denied her access to its services or engaged in conduct that would violate federal or Maryland consumer protection laws.

Colorado AG Targets Call Frequency and ‘Creditor-Branded’ Letters in Settlement with Collector

The Attorney General of Colorado has reached a settlement with a Texas-based collection company after an investigation found it allegedly sent letters that appeared to come directly from a medical provider and placed repeated collection calls beyond limits set by state law. The agreement resolves allegations that the collector used deceptive communication practices while collecting ambulance-related medical debts from Colorado consumers.

Judge Compels Arbitration in FCRA Case Over Repossessed Vehicle and 1099-C Dispute

A District Court judge in Arizona has granted a defendant’s motion to compel arbitration in a Fair Credit Reporting Act case involving a car loan that went south. What makes the ruling interesting is that the judge needed a 28-page order to lay out all the background and the reason why the motion to compel should be granted. At the center of the dispute was whether a borrower’s claims over repossession, credit reporting, and a canceled debt notice should be litigated in court or sent to arbitration based on language contained in the original vehicle financing contract.

ProPublica: Consumer Relief from Credit Bureau Complaints Drops Sharply as CFPB Enforcement Weakens

A new investigation from ProPublica is drawing attention across the consumer finance ecosystem after finding that two of the nation’s three major credit bureaus, TransUnion and Experian, are resolving far fewer consumer complaints in customers’ favor since the federal government began scaling back enforcement activity at the Consumer Financial Protection Bureau. The report suggests that the drop in consumer relief coincides with policy changes and staffing cuts at the agency that historically acted as a watchdog over the credit reporting industry.

RevCycle, Inc. Appoints Tracy Dudek as President to Advance Best-in-Class Revenue Cycle Performance

RevCycle, Inc., a national provider of healthcare revenue cycle management and receivables management services, today announced the appointment of Tracy Dudek as President, effective March 2, 2026. Dudek will report directly to Chief Executive Officer Brent Bergman and will oversee the organization’s operational strategy, client partnership initiatives, and performance optimization efforts.

WORTH NOTING: Stats about consumers with personal loans ... Why younger Americans are more optimistic about the economy ... A handful of ways that consumers are saving big at the gas pump in 2026 ... A lot of consumers have no idea what a FICO score is ... Design tricks to transform your home, according to a feng shui expert ... Questions to ask yourself before trying to be sarcastic ... A look at all the baggage that went unclaimed by travelers last year ... The most reliable ways to build confidence at work.

Trailer Tuesday, part I

Trailer Tuesday, Part II

Webinar Recap: Opening the Black Box: Making AI Decisions Transparent

Artificial intelligence is transforming credit and collections, but its growing complexity raises critical questions about fairness, compliance, and trust. In this webinar, panelists Jordan Akins (Kollx.ai), Chris Busse (SingleStone Consulting), and Saket Sahoo (Connect BPS) discussed the importance of explainable AI (XAI)—systems where predictions and decisions can be clearly understood and traced.

Jordan Akins illustrated XAI with a medical analogy: a doctor who explains a diagnosis inspires confidence, while one who cannot risks malpractice. Similarly, debt collectors must be able to explain AI-driven decisions to regulators, courts, and consumers. Chris Busse emphasized documentation and radical transparency, noting that “write it down” remains invaluable for accountability. Saket Sahoo urged organizations to focus on decisions rather than tools, stressing that poor data quality is often the root of flawed AI outcomes.

The panel warned of risks when AI outputs cannot be explained. Biased account scoring or settlement offers could trigger lawsuits under laws like ECOA or FCRA. Examples from other industries, such as Apple and Goldman Sachs’ $70M settlement over biased credit limits, highlight the stakes. Panelists agreed that explainability requirements vary by application: low-risk uses like call transcription may tolerate black-box AI, but high-risk decisions—such as dispute handling or settlement offers—demand transparency.

🧠 Key Takeaways:

Assess AI risk levels: Identify which applications (e.g., settlement offers, dispute handling) require explainability versus those where black-box AI may be acceptable.

Demand vendor transparency: Ask vendors if they conduct transparency audits and can explain their models beyond marketing hype.

Prioritize data quality: As Saket Sahoo noted, “If you don’t have accurate data, AI is not even for you.” Clean, reliable inputs are essential for trustworthy outputs.

This session underscored that explainable AI is not just a technical issue—it’s a business, regulatory, and consumer trust imperative for the credit and collections industry.

Did you know you can get full access to all of my past webinars, along with transcripts and summaries of each, for only $29/month? Sign up to be a premium subscriber today!

The Daily Digest is sponsored by TCN