- AccountsRecovery Daily Digest

- Posts

- Daily Digest - August 19, 2025

Daily Digest - August 19, 2025

Brought to you by: TCN | By Mike Gibb

Mike Gibb

August 19, 2025

The perception of the Consumer Financial Protection Bureau has changed radically in the first eight months of 2025. Now free to lay off up to 90% of its staff, the regulator has gone from being something that was whispered about in corners because people were afraid that mentioning its name would conjure up a CID or enforcement action out of thin air to the industry welcoming any news related to the Bureau because it usually has something to do with dismissing a lawsuit or stepping away from rulemaking.

Two former CFPB officials, John McNamara and Mark J. Cavin are going to be speaking at ComplianceCon next month, sharing stories on their time at the Bureau and their visions for the future of the agency. Sign up at https://compliance-con.com to get your front-row seat to that session and two dozen more, all aimed at helping compliance professionals from across the credit and collection industry stay on top of what's going on and provide best practices and actionable ideas to be more effective and efficient.

FDCPA Class-Action Filed Over MVN Date Issues

A collection operation is facing a class-action lawsuit alleging it violated the Fair Debt Collection Practices Act because the Model Validation Notice that was sent to the consumer used an itemization date that was the same date the letter was mailed to the consumer, yet still informed the recipient that fees had been incurred on the unpaid debt, amounting to 25% of what was owed.

This series is sponsored by WebRecon

A MESSAGE FROM TCN

TODAY‘S WEBINAR

UPCOMING WEBINARS

|  |

|  |

|  |

Court Rejects MTD, Says 1692e(8) Claim Doesn’t Require Written Dispute

A District Court judge in Georgia has denied a defendant’s motion to dismiss a Fair Debt Collection Practices Act, ruling that the plaintiff did not have to submit a dispute in writing in order to allege the defendant violated Section 1692e(8) of the statute.

DFPI Reaches $2.3M Settlement With Servicer for Overcharging Consumers

The California Department of Financial Protection and Innovation has reached a $2.3 million settlement with Caliber Home Loans, Inc., after finding the Coppell, Texas-based company overcharged nearly 5,000 borrowers in the state and failed to maintain proper trust account practices.

Volatility in Economy Shifts Credit Card Usage and Consumer Health

A new study from J.D. Power highlights growing financial strain among U.S. credit card customers, with more than half of cardholders carrying revolving debt and 56% classified as financially unhealthy. The findings reveal widening divides in consumer satisfaction and underline the pressure many households are facing in today’s economy.

WORTH NOTING: A new report from the U.S. Chamber of Commerce shows how small business are adopting the use of artificial intelligence ... Wage increases still are not keeping up with the pace of inflation, putting consumers in a deeper financial hole ... Credgenics, a debt collection technology software provider, has acquired a majority stake in an Indian collection operation ... Ten different use cases for artificial intelligence in debt collections ... The impact of financial dynamics on relationships is huge ... A psychiatrist shares how to reduce anxiety in 15 seconds with a breathing technique ... Which car models have the most comfortable seats? ... Why buyers are gaining the upper hand in the housing market.

Trailer Tuesday, part I

Trailer Tuesday, Part II

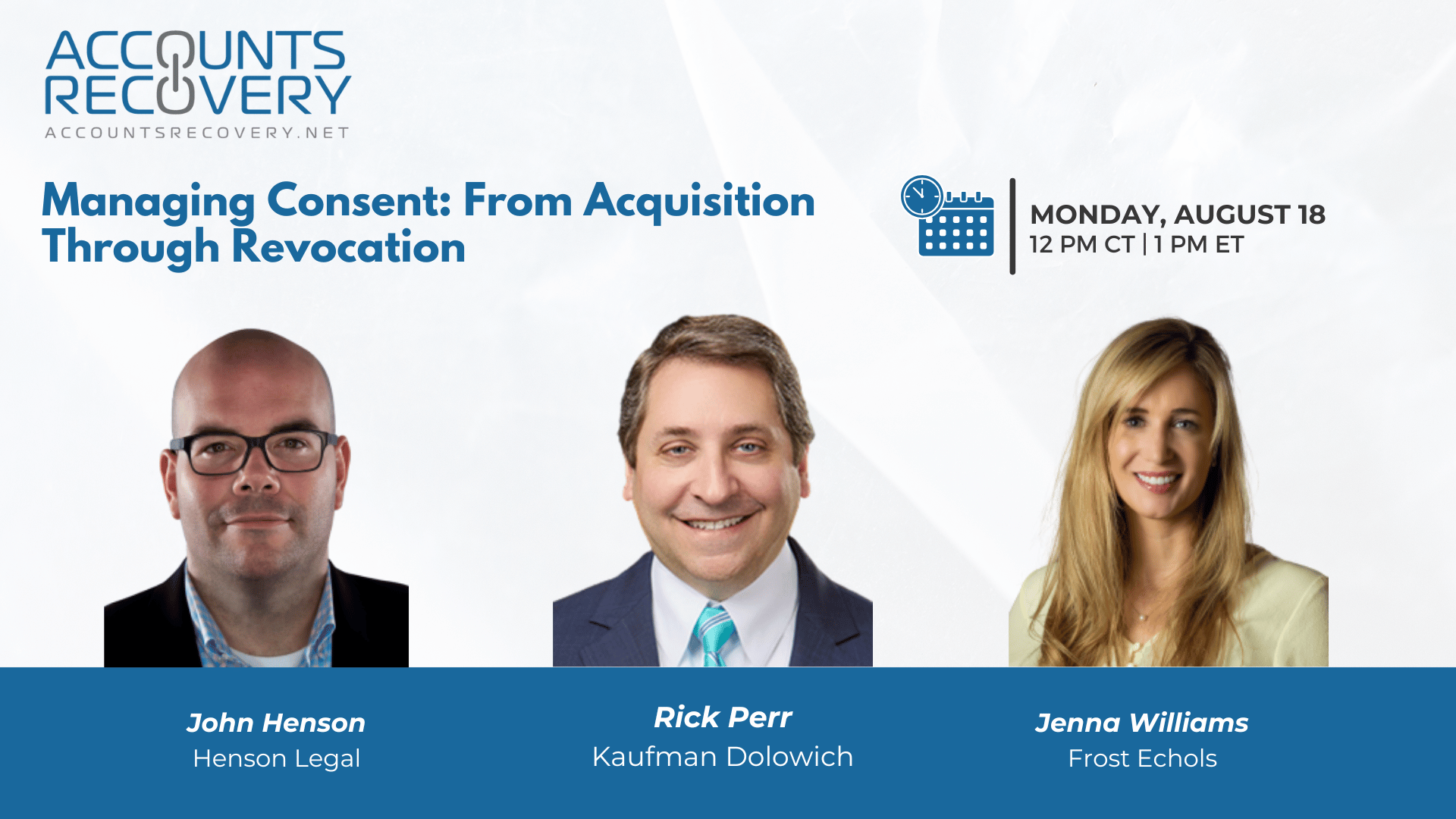

Webinar Recap: Managing Consent: From Acquisition Through Revocation

In today’s collections environment, consent is more than a compliance checkbox—it’s the foundation for consumer engagement and risk management. In a recent webinar hosted by AccountsRecovery.net, industry experts Rick Perr, John Henson, and Jenna Williams explored best practices for obtaining, tracking, and honoring consumer consent across multiple communication channels, while addressing the complexities of revocation.

The discussion highlighted that consent is not a “one-size-fits-all” concept. From TCPA requirements for calls and texts, to FDCPA restrictions on third-party communications, to state-level rules in places like New York and Washington, compliance demands careful differentiation. Panelists stressed that agencies must maintain flexible systems to code and track consent at various stages—from onboarding to active account management to dispute resolution.

Another key theme was revocation. The FCC’s recent clarification around “reasonable revocation” under TCPA requires agencies to quickly process opt-out requests, whether via phone, text, email, or mail. Failing to act promptly not only risks litigation but can damage consumer trust. Panelists also noted the growing role of AI in detecting revocation requests, while emphasizing that human oversight remains essential in ambiguous cases.

The bottom line: consent management is complex, but getting it right reduces legal exposure, saves time, and helps focus resources on consumers most likely to pay.

🧠 Key Takeaways:

Differentiate consent types: Understand the multiple “bubbles” of consent (TCPA, FDCPA, Regulation F, E-Sign, EFTA, state-level) and track them separately.

Act fast on revocation: Implement systems to process opt-outs in near real time—what consumers perceive as immediate action is critical to avoiding lawsuits.

Blend automation with oversight: Use technology (AI, CRMs, voice analytics) to flag and process revocations, but maintain human review to handle nuanced situations.

By proactively managing consent, agencies can navigate compliance risks while maximizing consumer engagement and recovery.

💡 For more events like this, visit accountrecovery.net or register for ComplianceCon—the industry’s only event devoted exclusively to compliance—this September in Nashville.

The Daily Digest is sponsored by TCN